In this review, I’ll present the highlights of what I said at the annual meeting of the service that held last week in Tel Aviv.

* * *

Five years ago, when you bought a value stock that is trading well below its fair value, a few years later it would have corrected up to the right price. In recent years, this logical process seems to have broken, and investors are motivated by something else. Looking at Tesla Motors sharp rise recently proves this point – investors are focused on growth and profits or valuation are not that important to them. You can ignore it and continue as usual, or understand the change and see how you can benefit from it.

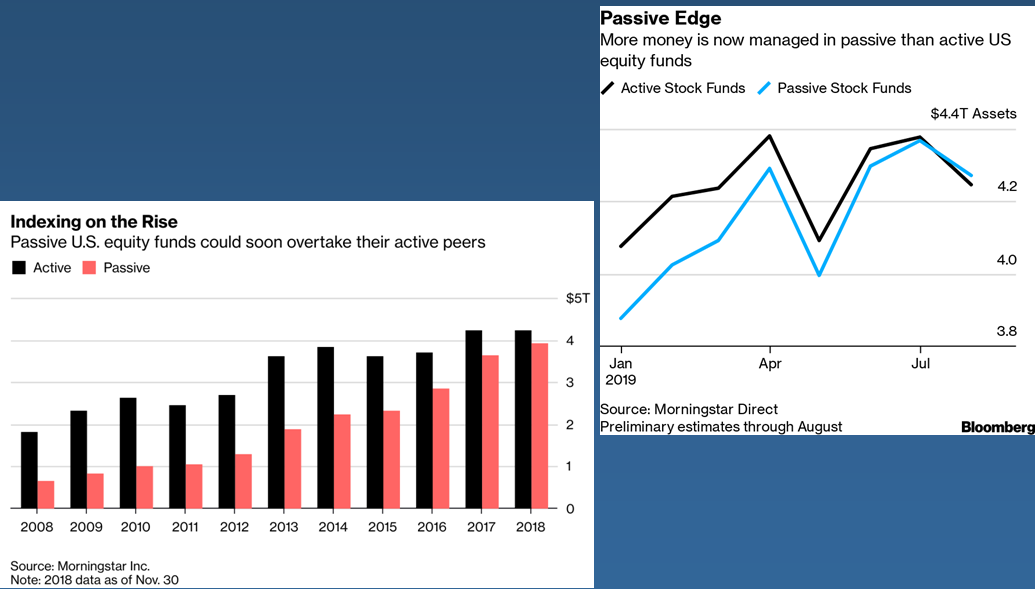

One of the key things that have changed is investors’ run from active investments to passive investments. Like I do in the LongRunPlan portfolio, in active investing you find an investment idea, analyze the company and estimate the value of the stock, and purchase it at a discount to its fair value. Then, you build a portfolio of 10-15 stocks, which are expected to increase more than the market average return.

On the other hand, in passive investing, companies and stocks are not examined in depth, but rather they all bought together, and this is the path most investors chose to go in recent years. Recently, the volume of passive funds (ETFs and index funds) crossed the $5 trillion and bypassed the volume of managed mutual funds.

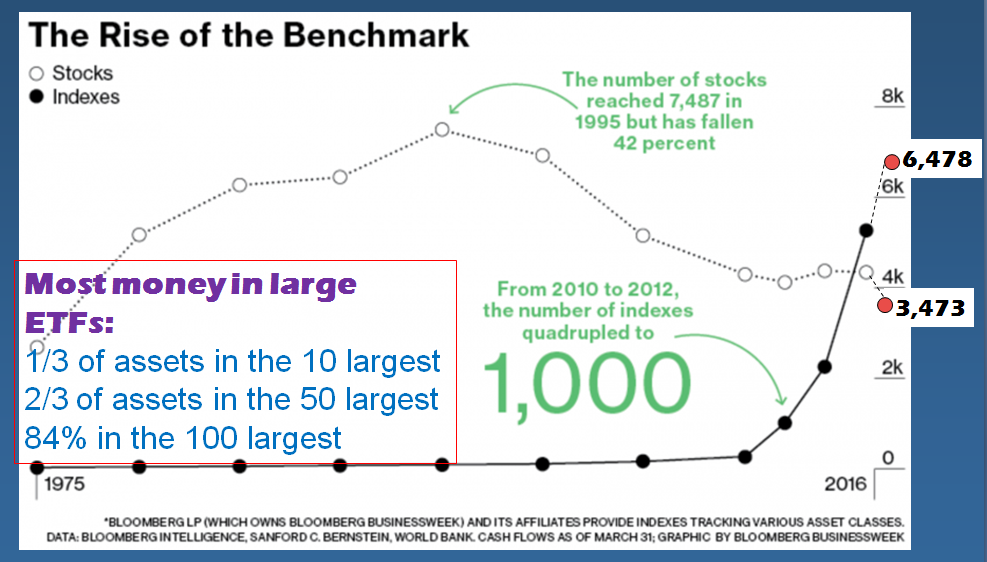

More indices than stocks…

What is more strange here is that there are currently more passive ETFs (funds that track a particular index, that is, buy all shares in the index) than American stocks. The number of US stocks (excluding foreign stocks) has recently fallen to 3,473 stocks while the ETF market grew to 6,478 index funds.

However, an analysis of the cash flow into these funds shows that most of the money is concentrated in the large funds, those that follow the leading indices – the S&P500, the Nasdaq 100 and leading global indices.

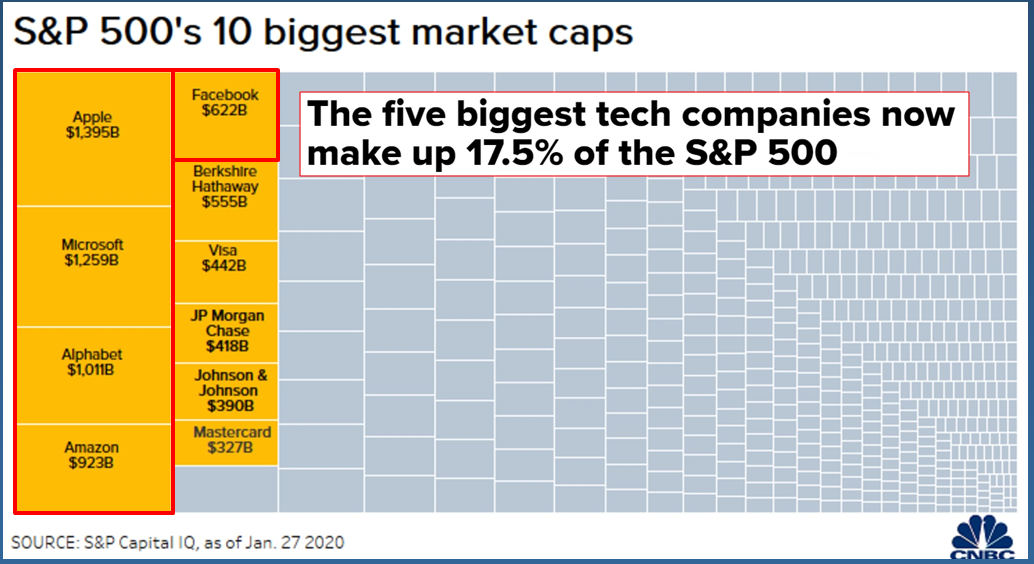

Investors prefer large companies

The thing is, the leading indices are dominated by a small number of giants. Microsoft, Apple Google, Amazon, and Facebook account for about 17.5% of the S&P500, and the top 10 US companies account for almost a quarter of the index. Think about it, 10 companies make up a quarter of the US economy. They are so big that except the Chinese stock exchange, they are bigger than all the companies together in any stock exchange you choose, which is a strange situation that has never been in history.

Investors’ run towards the indexes caused most companies in the leading indexes to rise sharply, sometimes for no specific reason. Take JNJ, for example, which grew by only 1.7% in the last quarter Year-over-year, but trades at a Price/Earnings multiplier of 27 (almost like Facebook with 25% YOY growth…). In contrast, the smaller companies, outside of the leading indices, remain behind, even if traded in unreasonable valuation.

The companies are also fueling this rally, by buying back their own shares on a massive scale, which had never been seen before. In the last 4 quarters, the S&P500 has made $700 billion in buybacks. Companies simply have a lot of cash that they have nothing to invest in, plus they can raise debt very cheaply and make buybacks, although their valuations don’t always justify it.

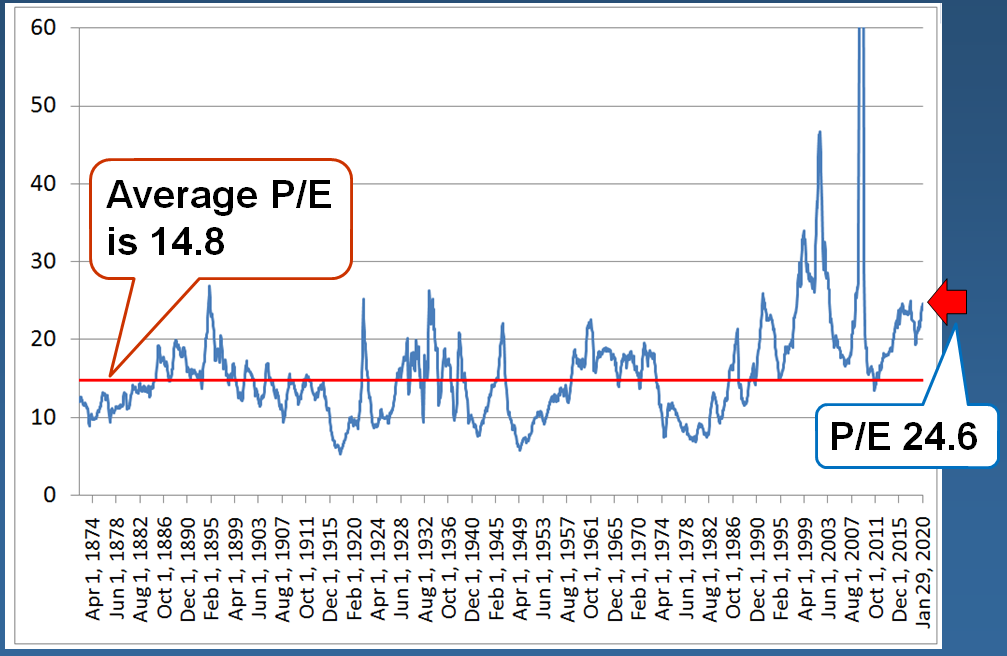

Is the stock market to expensive?

The question is, when trading at a P/E of 24.6, did the US stock market went up too high?

To answer this, we have to look at the bond market, which is the reference through which investors are valuing the stock market.

Ask yourself: “What annual return would you be willing to settle for in an ETF that tracks the S&P500 when the 10-year US treasuries are traded at 1.59%?”

Today, the S&P500 trades at a P/E of 24.6, i.e. at an Earning Yield (the inverse of the P/E) of 4.0%. This is about 2.4% above the long-term bond yield, which means investors are willing to settle for a 2.4% premium to take the risk of investing in the stock market.

That sounds a bit, but historically, it’s pretty much the excess return premium that investors demanded over the bond market. That means the indices are more or less valued where they should be. In simple words, the stock market is traded at its fair value and it’s certainly not in bubbly phase (but of course there are specific stocks that are very overvalued).

If interest rates in the US stay where they are, it implies that the indices don’t have much of an upside to rise from the current price (unless there is a significant growth in the companies’ profits), so I believe that the current valuation is preferable to active investment over passive investment in the indices.

However, recently we heard that the Fed is considering to reduce interest rates again in the near future. If we assume that the Fed lowers the interest rate by 0.25% and investors are willing to reduce the excess return premium over the bond market to 1.5%, for example, then we can easily justify a P/E of 34.4. This is a very extreme scenario, but it is not unlikely that it will occur in the current stock market euphoria. Contrary to current valuation which is relatively expensive but not a bubble, this extremely high valuation will place stock prices in a bubble zone.

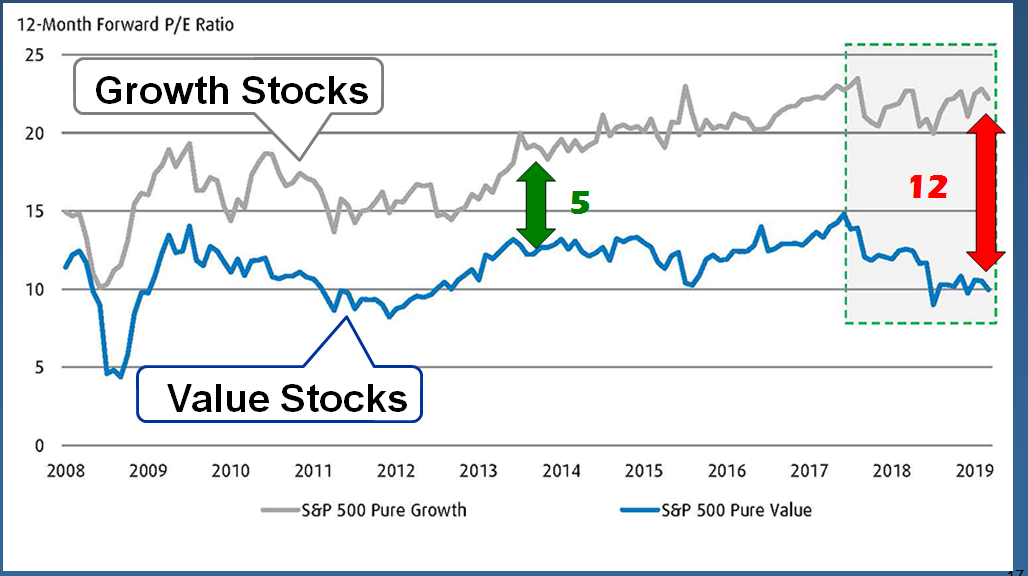

Growth or Value – What is better for us now?

The stock market is not evenly divided. Today, the gap between the valuation of growth stocks (high-growth companies) and value stocks (those trading below their economical value) is the highest in history.

Usually, the gap between the P/E growth stocks to value stocks is about 5 points, but today is more than double that value. I predict that this situation will not last for long – value stocks will trade up and growth stocks will correct down in the next few years.

The stocks in the LongRunPlan portfolio are even much cheaper than the average value stocks.

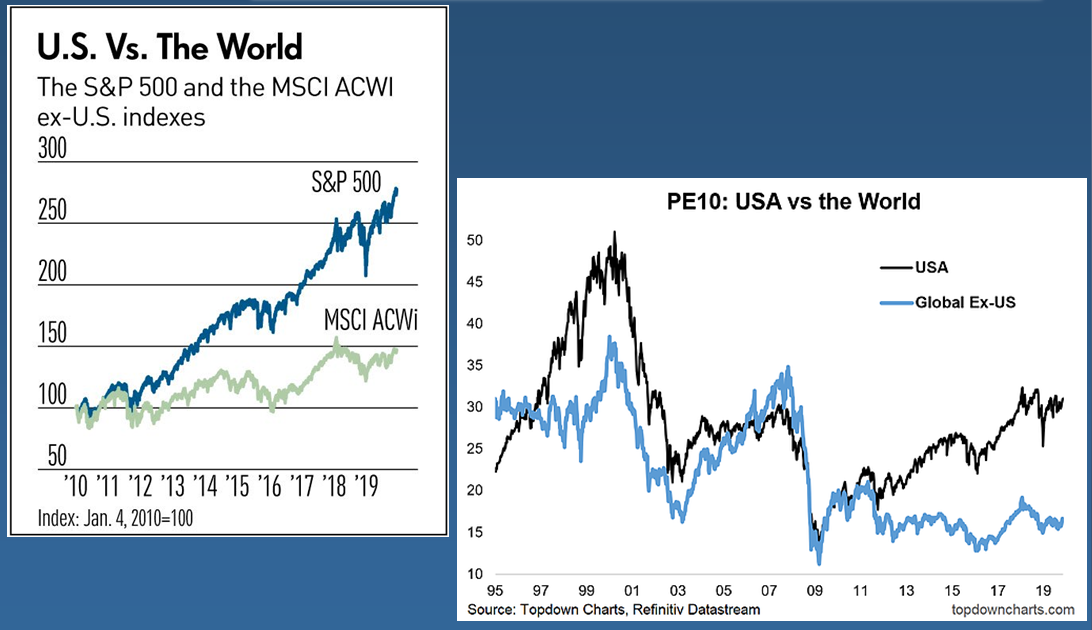

For general knowledge, the US market is currently the most expensive stock market in the world. Outside of the US, there are quite a few markets that are much more attractive. I’ll try to highlight some of the international attractive stocks that I like (for example, I hold E.N Shoham Business in the Hebrew version of the LongRunPlan portfolio. I think it will be at least doubled in the next 2 years. It is traded under the symbol KLIN-M at Interactive Brokers).

Summary

In my opinion, in the current period, it is essential to hold both traditional value stocks and growth stocks, and I intend to do so in the coming years. I just added a great growth stock to the portfolio and will keep looking for more attractive ideas. Also, I think it is wise to keep at least 15% of your money in cash that will be used when the market cools down a bit.

Continue to invest wisely and you’ll get a satisfactory return over the years.

Be the first to comment on "Market valuation: How much upside has left for stocks?"